Lithium saw its price triple in 2016, and cobalt—another massively important element in the lithium-ion battery—rose almost 50 percent in the same year, and is poised to become the next critical metal as the world sits on the edge of an energy revolution driven by mainstream electric vehicles, battery gigafactories and power walls.

Together, lithium and cobalt are the most alluring investment duo on the global market, and we’re only getting started. Supply is expected to be short, prices are expected to spike, and small-cap explorers are expected to emerge as key players as they secure new prospects from the U.S. state of Nevada, to Latin America’s ‘Lithium Triangle, to Ontario.

Against this dramatic backdrop, the strategic advantage is brilliant for new explorers like LiCo Energy Metals (TSX:LIC.V; OTCQB:WCTXF), which is targeting both of these critical commodities.

The lithium-ion batteries that are essential to the market-disrupting energy picture actually use more cobalt than lithium by weight, which means that ambitious plans to pump out volumes of EVs to meet growing mainstream demand all over the world could be at risk if new supplies are not secured.

Lithium Spot Prices Tripled in 2016, and Cobalt is Set to Rise Next

Commodities prices have been falling pretty much across the board, and particularly since the oil-price rout that began in the summer of 2014—but not lithium. In the past year, lithium spot prices have tripled, driven by growing demand for lithium-ion batteries and expected future demand. For November, 99.5 percent lithium carbonate China spot prices rose 0.15 percent, and stabilized at around US$18,000/tonne.

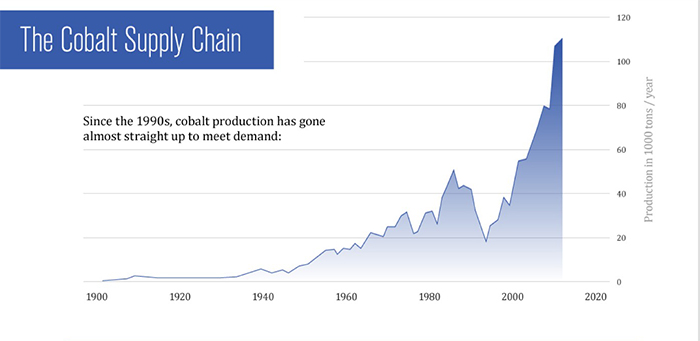

Cobalt spot prices increased 46 percent in 2016 thanks to growing demand and tight supply that has in part come about because of flat copper and nickel markets, and cobalt has largely been mined as a by-product of these two metals. In February 2016, cobalt was at US$10/lb, but by the middle of December it was over US$14.60/lb.

And current prices are further supported by temporary shutdowns at key mines. But it all means we’re looking at a deficit already in 2017, so it’s a tight market that can continue to support a jump in prices.

Most of the world’s cobalt supply comes from the Democratic Republic of Congo (DRC), and there is a problem meeting demand with or without the coming surge in battery demand. At the same time, supply from chaotic and unstable DRC is always uncertain. The race to secure cobalt supply chains is in full force.

Demand Set to Overflow

Between 2005 and 2015, global output rose by 20 percent - however, 2015 total demand only saw a small portion of the total coming from batteries. As more high quality lithium is needed for batteries, lithium demand will overflow in the coming years.

The 2016 surge in spot prices in China coupled with the ravaging hunger for lithium batteries and power storage solutions has triggered fears that we are on the edge of a major supply problem—but it’s a euphoric problem for lithium exploration companies and it has opened up the playing field to new entrants.

Tesla has stormed the mainstream U.S. market with its newest model; EVs have already entered the profit stage in Norway, and will soon be followed by the Netherlands, helped out by some EV-market-loving laws that demand that every single car in the country be electric by 2025. In Asia, too, EVs are bursting the traditional car bubble.

Volkswagen (OTCPK:VLKAY) is sure that a whopping 25 percent of its car sales by 2025 will be EVs, and the World Energy Council expects 1 in 6 cars sold in 2020 will be EVs. Finally, according to Bloomberg, by 2022 EVs will be cheaper than that natural gas brethren.

And with a mind-boggling 12 battery gigafactories on the books globally, we’re looking at a supply and demand equation that is overwhelming in favor of the new lithium miner. It’s not only Tesla: LG Chem (OTC:LGCEY, Foxconn, BYD (OCTPK:BYDDY) and Boston Power are all building new battery factories, too—among others. Imagine the manufacturing capacity here that requires monumental amounts of lithium and cobalt that we simply won’t have.

In 2015, the battery industry accounted for 35 percent of global lithium demand, according to the United States Geological Survey (USGS). More to the point, this industry bought 11,375 tonnes of refined lithium. Then we have cobalt, which is even more astonishing, considering that the battery gigafactories aren’t even online yet. According to the Cobalt Development Institute (CDI), the battery industry represented 41 percent of global cobalt demand in 2015, or about 40,600 tonnes.

By 2020, the production capacity of lithium batteries is set to TRIPLE:

The lithium ion battery market is forecast to expand to $46.2 billion through 2023, which represents an 11 percent average annual growth rate.

Lithium will be the biggest disrupter on the energy market, and this is probably the most important moment for both lithium and cobalt—the early-phase of the market disruption when investors can still get in for cheap, and the turning point where investments start to turn into profits.

This Segment is all About New Exploration

As future supplies of lithium and cobalt promise to fall well below soaring demand, the name of the game to is stake out new potential lithium acreage and get an early foothold on cornering the market share for what is no less than an energy revolution.

From an investor perspective, it’s not a game best played through the traditional big three lithium miners: Albermarle (NYSE:ALB) in Chile and Nevada; SQM (NYSE:SQM) in Chile; FMC (NYSE:FMC) in Argentina.

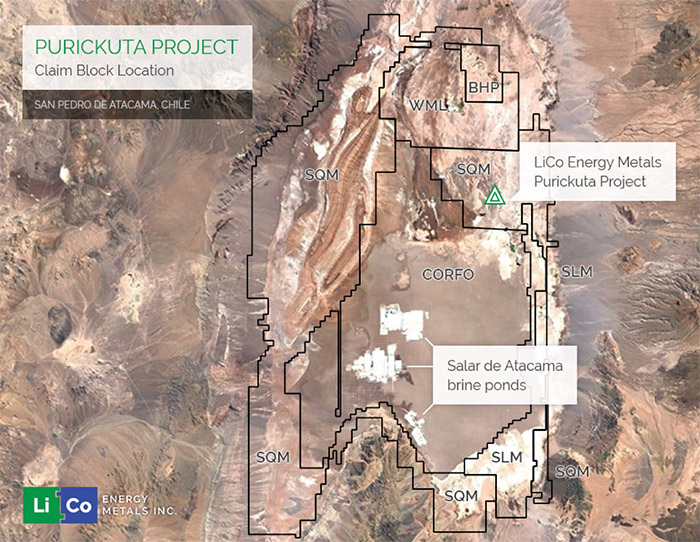

New supply is now critical, and it’s worth looking at an ambitious miner like LiCo Energy Metals, precisely because they’re focusing heavily on acquisitions in all the sweet spots, from cobalt in Canada to lithium in Nevada and Chile’s Salar de Atacama.

The land rush is already on in full force in Nevada, home to the only producing lithium mine in the U.S.--Albermarle’s Silver Peak Mine. This is where a lot of new entrants to the lithium game are clustering, not the least because it’s right in Tesla’s gigafactory backyard and Nevada’s geological picture tells us there’s a lot more lithium to be found.

The prospects are perhaps even more spectacular in Chile, which already supplies 37 percent of the world’s lithium, with low-cost, high-grade resources.

Then we have cobalt, which in the new exploration equation becomes even more valuable when you consider that almost 95 percent of global cobalt comes from copper and nickel mining, as a by-product. That makes its supply heavily dependent on copper and nickel demand and means it will be difficult to come by at a decent price.

The numbers speak for themselves. In 2015, the battery industry accounted for 41 percent of global cobalt demand, according to the Cobalt Development Institute (CDI). However, over the next 10 years, CDI expects that to increase to 65 percent, and it will be unsustainable unless new cobalt resources are brought into production.

It’s all about exploration right now, and particularly about explorers who are targeting new lithium and cobalt plays with an eye to becoming a key part of this energy revolution by cornering new supply for an explosive demand equation.

In the Lithium world, there are two places a mining company needs to be: The lithium Triangle between Bolivia, Chile, and Argentina, and the state of Nevada in the U.S. For Cobalt, we’re looking to Canada for new supply, and the best place to look for a new mine is beside an old one.

LiCo is ticking all three of these boxes. It ticks the first two boxes with two early-phase lithium exploration projects in the heart of the U.S. lithium rush in Nevada and a high-grade, advanced-stage cobalt project in the heart of a historical mining district in Ontario, Canada. The third box is probably the most exciting: LiCo has signed a letter of intent to option some prime lithium territory in Chile’s highly sought after Salar de Atacama in the “Lithium Triangle”, creating a major strategic advantage in the new supply game. (This recently announced property option in Chile is subject to TSXV approval)

LiCo’s high-grade, advanced-stage Teledyne Cobalt Project in a prime mining location in Ontario covers 11 claims over 1,368 acres, along with CAD$25 million in inflation-adjusted infrastructure. A CAD$700,000 exploration program is already underway here, and the company is cashed-up with CAD1.8 million in the bank. Uniquely, this is a 100 percent cobalt mine—and that’s exactly what the market wants to see right now.

In hot Nevada, LiCo has the Dixie Valley Exploration Project and the Black Rock Desert Project (subject to TSX Venture exchange approval) both early-stage conceptual lithium brine projects with 472 placer claims across more than 9,600 acres.

In Chile’s Salar de Atacama, where 37 percent of the world’s annual production of lithium comes from, LiCo’s Purickuta Project (pending TSX Venture exchange approval), is surrounded by major producers of the world’s cheapest and highest-grade lithium. This is a project that is close to everything that matters—major companies including SQM, producing 100 percent of Chile’s existing lithium output, pumping and solar evaporation installations, power, labor, transportation and other infrastructure. Here, the lithium world will be watching out for the quick definition of reserves and the fast-paced set-up of new production facilities.

So when anyone asks whether it makes sense for a junior to step into the cobalt game, the answer is a resounding yes—especially when we’re talking about a pure cobalt mine, which is difficult if not impossible to find these days, backed up by two lithium projects in the heart of the Nevada land rush, and a new fourth play (pending TSXV exchange approval) in Chile’s lucrative portion of the “Lithium Triangle”.

LiCo strategized itself right into the middle of this revolution.

Smart commodity investors will take on a new currency, and it will be cobalt and lithium, the backbone of the dreams of visionaries like Elon Musk, whose hard work is now a fundamental reality. The juniors who figure this out first will be rewarded mightily.

Legal Disclaimer/Disclosure: This piece is an advertorial and has been paid for. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this Report should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. We make no guarantee, representation or warranty and accept no responsibility or liability as to its accuracy or completeness. Expressions of opinion are subject to change without notice. We assume no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.