Precious and industrial metals have rallied as the dollar dives and global chaos rules the day. So, if you have stayed away from mining this year, it’s time to rethink your investment strategy.

Following the U.S. airstrike on Syria, precious metal prices have soared while industrial metals have been loving life since the U.S. presidential elections.

-

Gold and silver prices have been swinging upwards since mid-March.

-

Copper prices have rebounded from their lowest level in three months thanks to the weaker dollar and solid trade data from China indicating stronger demand.

-

Iron ore is the odd man out here because it’s entered a bear market over the past week thanks to uncertainty over Chinese reforms. But for the mining giants who are diversified, it’s worth waiting to see how it play outs. For the small iron ore miners, tough times are ahead.

-

Lithium is up over 400% and there is a veritable stampede to get in on the commodity that is feeding our electric vehicle hunger.

-

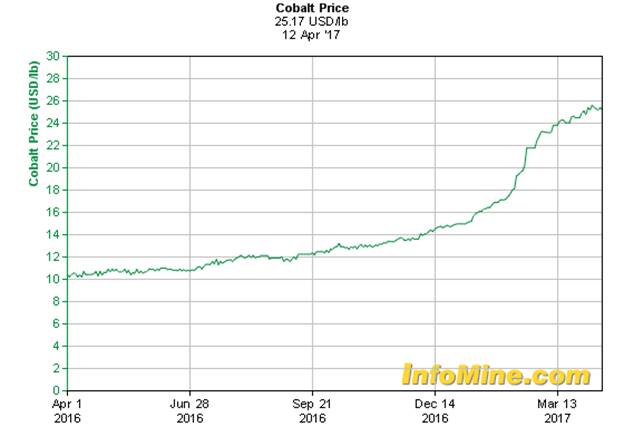

Cobalt stands to do even better, and because everyone’s been paying attention to lithium in this rush, the real money to be made is here. There isn’t enough, and what’s available is unethically sourced from the Democratic Republic of Congo (DRC). Cobalt has made gains for 24 straight weeks, and the sky is the limit on this one.

Here are our top 5 mining picks right now:

#1 Barrick Gold (NYSE:ABX)

This is a good short-term pick because gold is rebounding after post-election losses and the increasing global chaos—most notably U.S. air strikes in Syria and North Korea’s suggestions that it’s finger is on the nuclear button. It’s not clear yet whether this is a good bet long term, but for now, gold is loving the chaos more and more.

For Barrick—a $23.27-billion market cap company, and the world’s largest gold producer—the Chile deal with Goldcorp adds a very attractive package of underdeveloped gold to its portfolio. This could be a solid long-term play, as well, because Barrick has been one of the smartest in terms of reducing debt, cutting costs, and generating solid free cash flow. It has one of the lowest cost structures of all the big miners, and it even raised dividends for shareholders in the last quarter of 2016.

And there are plenty of catalysts even beyond broader gold fundamentals. Word is that Barrick is considering the sale of all or part of its Lagunas Norte mine in Peru, which is potentially worth anywhere from $700 million to $1.4 billion.

As gold climbs, Barrick is extremely well-positioned to make attractive gains.

#2 Scientific Metals (TSX.V: STM) (OTC: SCTFF)

As hedge funds start hoarding cobalt ahead of the demand surge and suppliers start panicking, Scientific Metals has stepped in with a major new acquisition in the prolific Idaho cobalt mining district.

Welcome to the Idaho cobalt belt, where, in September, Scientific Metals entered into an agreement to acquire the Iron Creek property, one of only two pure play cobalt companies that are drill ready, the other currently engaged in economic feasibility studies, allowing it to then go into production. This latter company is located in the same Idaho belt as Scientific Metals.

In this acquisition, Scientific Metals scooped up property that has already seen a substantial amount of historical exploratory work, including 30,000 feet of diamond drilling. Iron Creek has a historic resource of 1.3 million tons containing .59% cobalt with encouraging indications of up to 10 million tons.

This small-cap looks even better when you consider its management. CEO Wayne Tisdale and his team at Intrepid Financial have in recent years helped create $2.7 billion in value by building and financing 5 companies in completely different industries—and one of them was a homerun in the lithium space. We like the odds here because cobalt is already a clear winner: prices are climbing, supply is already short, and demand is set to explode. Scientific Metals is well-positioned to create shareholder value amidst this perfect storm.

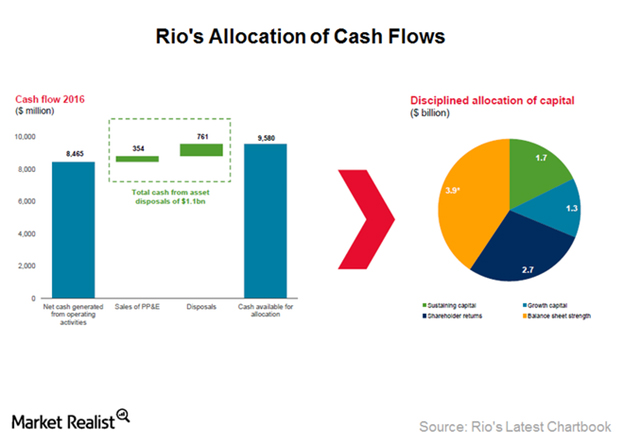

#3 Rio Tinto plc (NYSE:RIO)

Rio stands out right now against some of its peers (BHP Billiton NYSE:BHP, for one) because it doesn’t have the negative baggage that comes along with an incident like the 2015 Samarco mine disaster in Brazil. But Rio isn’t just a good bet by default, and thanks to the expensive legal quagmire of some of its peers: There are some attractive catalysts at play.

Rio is currently trading at a market cap of $68.91 billion.

Rio makes most of its revenue from iron, but it’s got new mines slated to come online over the next few years, including an iron ore mine in Australia that is expected to start producing in the fourth quarter of this year. This is a great pipeline of new projects, in fact. A second mine (bauxite) in Australia is scheduled to come online in the first half of 2019. Further down the line, in 2020, Rio expects to start exporting its first copper from its Mongolia mine.

Last year, the company moved to increase dividend, and shareholders appreciate the return of value.

Its stock has also stood up to its peers. In the first quarter of this year, Rio stock gained 5.8%, while BHP Billiton’s gained only 1.5%. Why? An increase in iron ore and coal prices, which balanced out any weakness Rio felt from aluminum and copper.

Rio has a solid balance sheet, with revenues outpacing costs and a clear and visible trend toward expansion.

#4 Teck Resources Ltd. (NYSE:TECK) (TSX:TECK.B)

If it’s sheer diversification that comforts you, Teck Resources is a great bet. All three of its core target metals (metallurgical coal, copper and zinc) have seen price rebounds.

Last year saw a solid coal rally thanks to Chinese moves to limit the number of days mines can operate in a year. This took a lot of pressure off supply, and prices responded nicely. In fact, it went from oversupply to tight supply, pushing coal prices from $90 to over $300 in November, which later dropped to about half when China stepped in to ease its restrictions in an attempt to rebalance the market. But Teck had already benefitted nicely, as shown in its Q4 results. Teck sells most of its coal on quarterly contracts, and was expecting even better results in Q1 2017.

Teck also benefitted from a big run for zinc last year.

But what we really like is its further diversification: Now it is getting into oil sands and it has shown financial and managerial savvy in its efforts to meet the development costs of its Fort Hills Oil Sands project, which expects its first oil by the end of this year. This is important because this play has a 50-year reserve life. It’s a pretty good time to get in on Teck, before this oil starts flowing.

#5 Albemarle (NYSE:ABL)

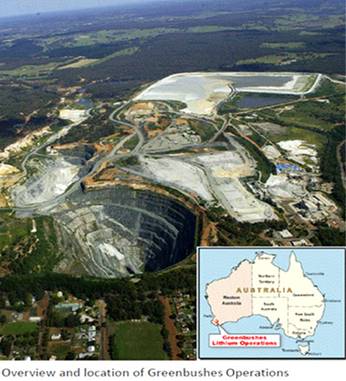

We like chemicals-maker and mining giant Albemarle for its lithium. Catalysts include Australia’s recent approval of the expansion of the company’s lithium concentrate production at its Greenbushes mine—the biggest active lithium mine in the world.

This move will more than double the lithium carbonate equivalent capacity at the mine from 80,000 metric tons per year to more than 160,000 metric tons. Albemarle should start commissioning the expansion in the second quarter of 2019.

Albemarle’s big push now is all about lithium—and meeting a massive future demand spike, sparked by an energy revolution that is in part driven by the introduction of electric vehicles to the masses.

This is an $11.74-billion market cap company with a lot going for it.

It’s a push that’s been very good to Albemarle. Its shares have gained 72 percent in a year, and it has outperformed analyst expectations and earnings for at least four consecutive quarters.

Honorable Mentions…

-

Hecla Mining (NYSE:HL): 2016 was a big year for Hecla (market cap US$2.04 billion), with silver production up 48% and gold up 24%, though 2017’s production targets won’t be as big.

-

Eldorado Gold (TSX:ELD): With a market cap of US$2.3 billion, this company didn’t benefit from the late-2016 rally because of concerns about production and performance of its operations; but it’s on track and the price is nice.

-

B2Gold (TSX:BTO) (NYSEMKT:BTG): This is a CAD$3.68-billion market cap company, and the one of the most actively traded companies on the TSX, and its stocks are climbing.

-

Alamos Gold Inc. (NYSE:AGI) (TSX:AGI): Alamos Gold, with a market cap of US$2.47 billion, is also set to outperform.

-

Fortuna Silver Mines Inc. (TSX:FVI): Catalysts included work on a feasibility study prepared in 2016 in Fortuna’s 100% owned Lindero gold project in Argentina’s Salta Province.

-

Pan American Silver Corp. (NASDAQ:PAAS): Attractive valuation relative to peers has led analysts to upgrade shares to outperform in March.

Legal Disclaimer/Disclosure: This piece is an advertorial and has been paid for. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this Report should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. We make no guarantee, representation or warranty and accept no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Baystreet.ca only and are subject to change without notice. Baystreet.ca assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.