While the beginning of 2016 was a rough one for metals miners, by the end of last year the recovery had started, and now we’re heading into a nice bull run at a time when mining stocks are still attractively priced.

We’ve seen a lot of smart restructuring, cost-reduction, debt pay downs, divestment and positioning. What the sector does next is critical, and these are our 5 top picks for gold, silver, copper and lithium in the coming weeks and months.

For gold, silver and copper, the Fed’s recent interest rate hike will boost prices. For copper particularly, this is an exciting time because the metal is getting a boost from two other major drivers: Trump’s $500-billion to $1-trillion planned infrastructure spending and what looks sets to be another Chinese run on the metal and another round of hoarding. For Lithium, the sky’s the limit as the energy revolution brings this metal into urgent focus.

We’re looking at solid growth strategies, smart management and the ability to strike the right balance. And it would be remiss to overlook the TSX lists because, in this sector, they shine. They have impressive access to capital—enough so that 57 percent of mining financings the world over were on the TSX and TSXV last year. They also have extremely liquid trading and a lot of growth potential.

Top 5 Mining Picks for Q1/Q2 2017

#1 Barrick Gold (NYSE:ABX)

Barrick—a $23.27-billion market cap company--is a solid long-term play not only because it’s the largest gold producer in the world, but also because it’s made significant moves to reduce debt, cut costs and generate solid free cash flow. The fourth quarter of 2016 even saw it raise dividends for shareholders.

Of all the big miners, Barrick has one of the lowest cost structures.

And there are plenty of catalysts even beyond broader gold fundamentals. Word is that Barrick is considering the sale of all or part of its Lagunas Norte mine in Peru, which is potentially worth anywhere from $700 million to $1.4 billion.

As gold climbs, Barrick is extremely well-positioned to make attractive gains.

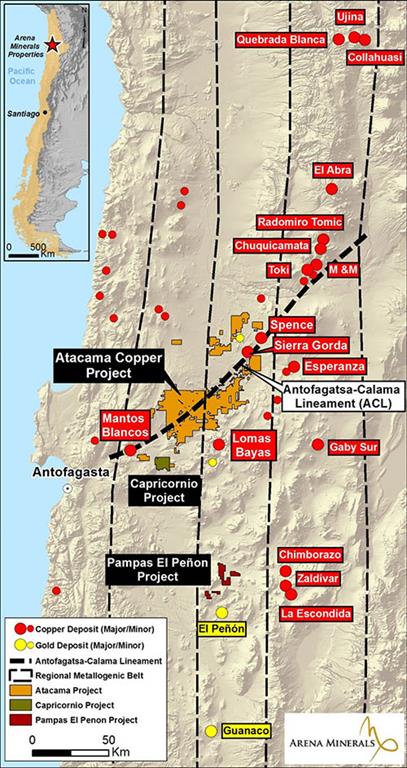

#2 Arena Minerals Inc. (TSX:AN.V; OTC:AMRZF)

Arena has accomplished what can only be considered a mining coup in the best copper venue in the world—Chile. When Chilean mining giant SQM came under pressure to finally give up some of the 4 million hectares of mining territory it controls in the country, Arena got there first, scooping up huge parcels of land in the prime copper and gold districts. All of this was untouched because SQM was focusing on lithium, potash, iodine and nitrate.

Arena’s flagship Atacama Copper project is an original 2,930-sq km exploration venue surrounded on all sides by some of the biggest operating mines in the world, with a ton of infrastructure in place. The company has secured 73,000 hectares in the heartland of the prized Antofagasta mining district, and it’s poised to potentially make the world’s next big copper discovery at a time the fundamentals are lining up strongly in favor of the metal.

The catalysts here are phenomenal and urgent. Just over 10 days ago, Arena was granted all of its environmental and drilling permits for 241 drill holes. And it’s scheduled to go down at breakneck speed, with the first 15,000 meters slated for completion by the end of April.

The company has cash on hand and a low burn because JV deals are doing the heavy financial lifting. This is a small-cap with a large-cap play, but the $10-million market cap company could move dramatically northwards in a matter of weeks as the drilling frenzy starts.

#3 Freeport McMoRan (NYSE:FCX)

Freeport—an $18.17-billion market cap company, is another favorite for copper, though it’s having some labor problems at its Cerro Verde open-pit copper mine in Peru. Further downward pressure has come from complications at its giant Grasberg mine in Indonesia. But this latter, at least, may be about to change.

Source: AsiaNews

This week, Freeport announced the restart of copper concentrate production at Grasberg. It hasn’t done wonders for the share price—yet, but it bodes well for the giant.

Freeport is the world’s largest publicly traded copper producer, the world’s largest producer of molybdenum, and a significant gold producer.

#4 Albemarle (NYSE:ABL)

We like chemicals-maker and mining giant Albemarle for its lithium. Catalysts include Australia’s recent approval of the expansion of the company’s lithium concentrate production at its Greenbushes mine—the biggest active lithium mine in the world.

This move will more than double the lithium carbonate equivalent capacity at the mine from 80,000 metric tons per year to more than 160,000 metric tons. Albemarle should start commissioning the expansion in the second quarter of 2019.

Albemarle’s big push now is all about lithium—and meeting a massive future demand spike, sparked by an energy revolution that is in part driven by the introduction of electric vehicles to the masses.

This is an $11.74-billion market cap company with a lot going for it.

It’s a push that’s been very good to Albemarle. Its shares have gained 72 percent in a year, and it has outperformed analyst expectations and earnings for at least four consecutive quarters.

#5 First Majestic Silver (NYSE:AG)

We love Mexico for silver, and Mexican silver has been great to First Majestic Silver—a $1.36-billion market cap miner that has seen an over 200 percent jump year-to-date.

The company focuses solely on Mexican silver, and the narrow focus has allowed it to overtake its peers. In total, First Majestic has six producing silver mines in Mexico and its operating results have been great. Combined with a strong balance sheet, this is a good bet for 2017.

There are also a number of catalysts, including upgrades at its La Encantada mine that could add another 1.5 million ounces of silver to its annual production. It’s also looking to expand its La Guitarra mine to 1,000 tons per day. This alone could double its production at reduce costs—two things any investor wants to see these days.

And, right now, its stock is low at $8—way down from earlier highs, so it’s a good time to get in on a solid strategy.

Honorable Mentions:

- Hecla Mining (NYSE:HL): 2016 was a big year for Helca, with silver production up 48% and gold up 24%, though 2017’s production targets won’t be as big.

- Pan American Silver Corp. (NASDAQ:PAAS): Attractive valuation relative to peers has led analysts to upgrade shares to outperform in March.

- B2 Gold (TSX:BTO) (NYSEMKT:BTG): This is the one of the most actively traded companies on the TSX, and its stocks are climbing.

- Teck Resources Ltd (NYSE:TECK)(TSX:TECK): This company’s copper deal with Arena is Chile’s Atacama is attractive, it’s also been doing a create job of cost-reduction and has low legal liability compared to some of its rivals.

- Gold Corp Inc (NYSE:GG): Gold Corp has seen lowering shares for the past three years, but it’s now clearly on the rebound, with stocks climbing and management working hard at increasing shareholder value.

- Alamos Gold Inc. (NYSE:AGI) (TSX:AGI): Alamos Gold, with a market cap of $2.47 billion, is also set to outperform.

- Fortuna Silver Mines Inc. (TSX:FVI): Catalysts included work on a feasibility study prepared in 2016 in Fortuna’s 100% owned Lindero gold project in Argentina’s Salta Province.

Legal Disclaimer/Disclosure: This piece is an advertorial and has been paid for. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this Report should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. We make no guarantee, representation or warranty and accept no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Baystreet.ca only and are subject to change without notice. Baystreet.ca assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.