The US digital advertising industry has officially crossed the $100-billion mark, making it bigger than TV, radio and print media advertising.

As this growth continues, a remarkable transformation is taking place within the industry, with the massive Google-Facebook advertising duopoly facing an existential challenge.

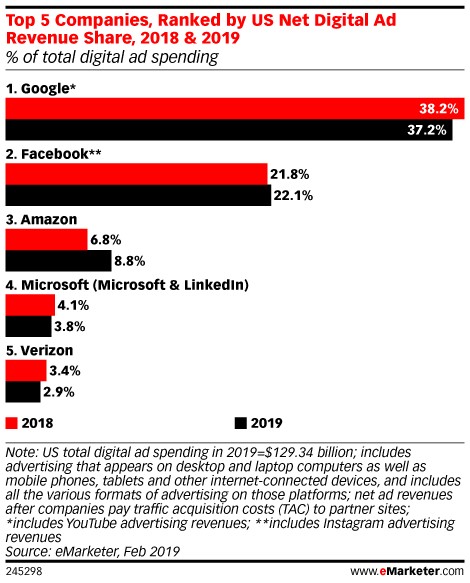

eMarketer is forecasting that the industry will top $170B by 2021. And with Google and Facebook currently hogging 60 percent of the market, American publishers and other media outlets are now fighting back.

Google made $4.7 billion in revenue from news content in 2018, while the entire news industry together only netted $5.1 billion. That’s over 2,000 news publishers combined.

Publishers everywhere are struggling. They’re simply not growing at all. They’re merely surviving. And it’s all because of the mountains of first-party data that they’re not collecting because they don’t have a platform to monetize it.

They’re under immense pressure to grow ad revenues, yet they are beholden to the likes of Google.

And while Google and Facebook are facing plenty of opposition, including being called before Congress, publishers won’t wait for some legal loophole to fix all of their problems.

Their survival depends on the quiet (until now) rise of new content management and data-collection platforms that can rewrite the rules of who gets rich off of advertising.

The future of publishing is designed to bypass the so-called digital giants, but in the meantime, there are also some other giant players encroaching on the digital ad duopoly.

Here are 5 companies that are ready to disrupt Google’s hegemony and re-write the advertising industry playbook.

#1 Amazon, Inc. (NASDAQ:AMZN)

A few years ago, trying to claw respectable market share from the industry heavyweights seemed like a really long shot.

Yet, Amazon is now on course to claim $10B, or nearly nine percent, of ad dollars in 2019 with Pivotal Research predicting a $38B haul for the company in 2023.

Amazon seems to be hitting all the right buttons…

The retail giant understands how Google, Microsoft, and Apple leverage advertising. They are just doing it in more aggressive, more profitable ways.

The giant online retailer has perfected the art of leveraging website real estate to display highly targeted ads to its 2.3B users.

As a result, nearly 50 percent of online product searches are conducted on Amazon’s website.

Amazon is also pushing hard into mobile video ads--a direct attack on Google

It’s even allowing brands to track traffic from Facebook in its latest push to cozy up to big marketers.

With Amazon’s high-margin cloud business, AWS, in the pink of health, Amazon certainly has the wherewithal to take on the digital ad giants head-on.

AMZN stock has climbed 18.3 percent in the year-to-date and 420 percent over the past five years thus making it a bit pricey. But with the digital ad gravy train served up, this stock still looks like a buy.

#2 Frankly Inc. (TSXV:TLK; OTCQX: FRNKF)

This is the upstart everyone should be talking about when it comes to challenging the digital ad duopoly.

This little-known company is a data-hungry content management company that reaches 100 million people and 75% of American households.

It’s entered the fray with a data solution that could give the biggest Western publishers the tools they need for digital advertising independence—with a ton of upside to boot.

Frankly offers broadcasters, media companies and publishers a platform for managing and monetizing all of their content and collecting targeted data from each of their users. Right now, it is the only company of its kind out there, and some very big names - including CNN and Vice - are already customers.

Frankly aims to shift the percentage of digital ad dollars by slipping in through the back door of this lucrative market, through the biggest mainstream publishers.

Google doesn’t even produce any news, yet it’s raking in all the revenues. That’s a tough pill for publishers to swallow.

Frankly’s answer? To offer publishers all the tools they need not only to create their ad revenue, but also to follow the upside with massive, first-party data collection that, when you add it up, is worth about $175 per person. That’s a gold mine for publishers who barely stay afloat while Google gets rich on their content.

Are publishers desperate enough to take on Google?

You can bet on it.

That’s why Newsweek just signed a deal with Frankly that’s designed to help the news major turn the tables.

But it’s just as big a deal for Frankly because it means that Frankly will be running all the information capture operations on Newsweek and doing all of Newsweek’s ad sales. It will grow Newsweek’s ad revenue by tens of millions of dollars, which all goes through Frankly in the end.

For Frankly, this is a $50M, multi-year service agreement with one of the biggest news producers in the world. But it also means first-party data access to Newsweek’s 40 million monthly active users.

This is a milestone in the industry because it’s the first partnership of its kind—ever— and it demonstrates the value of leveraging a fully integrated multi-media platform such as Frankly’s.

Frankly has 100+ million active users across its network, and’s just signed a $50-million, multi-year deal with giant Newsweek, which will add 40 million more.

It also recently hooked CNN and VICE in its deal to acquire Vemba’s advanced video technology.

For a company with a market cap of only $30 million, harnessing the priceless first-party data of 75% of this country, undervaluation isn’t much of a stretch of the imagination until the news flow starts to catch up with the first-data bounty, starting with Newsweek.

That’s when Google might wonder who’s behind this tiny data hog that no one’s ever heard of.

#3 Verizon Communications Inc. (NYSE:VZ)

In 2017, Verizon acquired Yahoo and AOL in a bid to create a rival ad sales business to Google and Facebook.

Verizon Media (formerly Oath) now houses popular brands such as The Huffington Post, TechCrunch and Yahoo Sports which collectively attract ~210 million monthly users.

From a financial viewpoint, the business has not been a resounding success with Verizon declaring a huge $4.6B writedown of its media properties last year--essentially declaring them nearly worthless.

Nevertheless, Verizon Media’s value proposition remains intact: more transparency and accountability in advertising. By focusing on high quality, professionally produced content and products, Verizon Media has been trying to avoid the same scrutiny faced by its bigger competitors, who struggle to stem the tide of fake news and violent videos.

With the Association of National Advertisers estimating that fraudulent, bot-driven traffic costs the industry ~$7B every year, Verizon Media will continue having its takers.

#4 Yelp Inc. (NYSE:YELP)

Yelp is a leading provider of user reviews and profiles on local businesses , primarily restaurants and home services. If there’s any media company that learned the hard way just how easy Google can destroy your business model, it’s Yelp.

A couple of years ago, Google arbitrarily changed its search algorithm leading to Yelp traffic slowing sharply almost overnight. Being a company that generates majority of its revenue from sale of ads on its Website to national brands and local businesses, Yelp’s top-line took a heavy hit and the company has been struggling to get back to its glory days.

Nevertheless, Yelp remains a popular consumer site especially for restaurant reviews. Beyond that, it has evolved into one of the very few review sites with a high consumer confidence score. It’s quite likely that over time, the company’s clout with consumers will help it regain favor with the investing universe.

If you love a turnaround story, then you might find Yelp an interesting value stock especially with the shares trading at a cheap 2x forward revenue.

#5 Snapchat Inc.(NYSE:SNAP)

Source: CNN Money

SNAP stock has been enjoying an annus mirabilis, rallying more than 200 percent at one point this year and more than 50 percent over the past 12 months.

Snapchat is another compelling turnaround story with two consecutive quarters of user and earnings growth helping to return it to Wall Street’s good books.

What’s particularly exciting about this company is that it appears to have impressive growth runways considering that comparable messaging apps like WhatsApp and Instagram (both owned by Facebook) boast 1B users apiece to Snap’s 190M. Further, Snapchat has also shown a willingness to think outside the box with its new augmented reality (AR) advertising products.

Another quarter or two of demonstrated user growth and SNAP stock might be able to definitively break above its 2017 IPO level for the first time.

Other companies taking the tech sector by storm:

Sandvine Corporation: Ontario is seeing some vibrant cybersecurity growth, as well. Sandvine corp. is engaged in the development and marketing of network policy control situations for high-speed fixed and mobile Internet service providers. Products include Business Intelligence, Revenue Generation, Traffic Optimization and Network Security.

Pivot Technology Solutions Inc. (TSX:PTG): Pivot focuses on the strategy to acquire and integrate technology solution providers, primarily in North America. It sells and supports integrated computer hardware, software and networking products for business database, network and network security systems.

With the energy sector becoming increasingly vulnerable to cyberattacks, companies like Pivot will see more and more attention from investors over time.

Absolute Software Corporation (TSX:ABT): This Vancouver-based company offers endpoint security and data risk-management solutions, and this year has seen a share price jump. Revenues are also up, and it looks like it’s on a path of securing strong new customers. The pipeline looks great, and forecasts for next year have been increased.

With strong management and an innovative team, Absolute Software is drawing growing investor attention. Absolute has seen a strong stock growth year to date and is expected to see strong growth as the cyber security market grows at a rampant pace.

Glance Technologies (CSE:GET) is a FinTech firm from a Vancouver entrepreneur who is gunning for a repeat of his earlier success, PayByPhone, a mobile parking payment system that took the market by storm before this was even a trend.

Glance’s biggest product, GlancePay, is a streamlined multi-platform mobile payment application which allows users to pay bills and earn rewards. And with a strong of positive news in recent weeks, investors are really beginning to pay attention to this growing Canadian tech company.

Mogo Finance Technology Inc. (TSX:MOGO): This is a new spin on unsecured credit, which is a burgeoning sub-segment of FinTech. Providing loan management, the ability to track spending, stress-free mortgages, and even credit score tracking, Mogo is at the forefront of an online movement to assist users with their financial needs.

Mogo’s software analyzes borrowers instantly and greatly reduces the traditionally cumbersome underwriting process for loans. It’s online only, so there’s very low overhead and a ton of cash to spend on marketing. Labeled as “the Uber of finance” by CNBC, Mogo is definitely turning heads.

By. Angel Rodriguez

IMPORTANT NOTICE AND DISCLAIMER

PAID ADVERTISEMENT. This communication is a paid advertisement. Safehaven.com, Leacap Ltd, and their owners, managers, employees, and assigns (collectively “the Publisher”) is often paid by one or more of the profiled companies or a third party to disseminate these types of communications. In this case, the Publisher has been compensated by Frankly, Inc. to raise public awareness of the company and to advertise and market the company’s products and services. Frankly paid the Publisher fifty thousand US dollars to produce and disseminate this and other similar articles and certain banner ads. This compensation should be viewed as a major conflict with our ability to be unbiased.

Readers should beware that third parties insiders and/or their affiliates may liquidate shares of the profiled companies at any time, including at or near the time you receive this communication, which has the potential to hurt share prices. Companies profiled in our articles frequently experience a large increase in volume and share price during the course of public awareness marketing, which often ends as soon as the public awareness marketing ceases. The public awareness marketing may be as brief as one day, after which a large decrease in volume and share price may likely occur.

This communication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. Neither this communication nor the Publisher purport to provide a complete analysis of any company or its financial position. The Publisher is not, and does not purport to be, a broker-dealer or registered investment adviser. This communication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor and only after reviewing the financial statements and other pertinent corporate information about the company. Further, readers are advised to read and carefully consider the Risk Factors identified and discussed in the advertised company’s SEC, SEDAR and/or other government filings. Investing in securities, particularly microcap securities, is speculative and carries a high degree of risk. Past performance does not guarantee future results. This communication is based on information generally available to the public and on an interview conducted with the company’s CEO, and does not contain any material, non-public information. The information on which it is based is believed to be reliable. Nevertheless, the Publisher cannot guarantee the accuracy or completeness of the information.

SHARE OWNERSHIP. The owner of Safehaven.com owns shares and/or stock options of the featured companies and therefore has an additional incentive to see the featured companies’ stock perform well. The owner of Safehaven.com has no present intention to sell any of the issuer’s securities in the near future but does not undertake any obligation to notify the market when it decides to buy or sell shares of the issuer in the market. The owner of Safehaven.com will be buying and selling shares of the featured company for its own profit. This is why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.

FORWARD LOOKING STATEMENTS. This publication contains forward-looking statements, including statements regarding expected continual growth of the featured companies and/or industry. The Publisher notes that statements contained herein that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect the companies’ actual results of operations. Factors that could cause actual results to differ include, but are not limited to, changing governmental laws and policies concerning, among other things, data protection and data privacy, the size and growth of the market for the companies’ products and services, the companies’ ability to fund its capital requirements in the near term and long term, pricing pressures, etc.

INDEMNIFICATION/RELEASE OF LIABILITY. By reading this communication, you acknowledge that you have read and understand this disclaimer, and further that to the greatest extent permitted under law, you release the Publisher, its affiliates, assigns and successors from any and all liability, damages, and injury from this communication. You further warrant that you are solely responsible for any financial outcome that may come from your investment decisions.

TERMS OF USE. By reading this communication you agree that you have reviewed and fully agree to the Terms of Use found here http://Safehaven.com/terms-and-conditions If you do not agree to the Terms of Use http://Safehaven.com/terms-and-conditions, please contact Safehaven.com to discontinue receiving future communications.

INTELLECTUAL PROPERTY. Safehaven.com is the Publisher’s trademark. All other trademarks used in this communication are the property of their respective trademark holders. The Publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the Publisher to any rights in any third-party trademarks.